AppLovin: Why Meta Just Strengthened the Bull Case

Short-seller attacks, an active SEC investigation, explosive growth and a premium valuation — separating noise from reality.

Prefer listening over reading?

I’ve added a short podcast-style audio summary below — perfect if you want the key ideas in a more relaxed format.

AppLovin (Ticker: $APP) has become one of the most controversial growth stories in the market.

After a massive run-up, the stock was hit by several short-seller attacks, questioning parts of the company’s advertising practices, the sustainability of AXON’s performance, and the quality of the growth behind the numbers. At the same time, the valuation had already reached a level where almost everything had to go right.

That combination is dangerous.

When a stock is priced for perfection, even a small crack in the narrative can be enough to trigger a sharp reset. And in AppLovin’s case, the market did not just question the valuation. It started questioning the engine behind the entire investment case.

But this is also where the story gets interesting.

A high valuation alone does not make a stock overvalued. Great businesses rarely look cheap when their fundamentals are accelerating. Peter Lynch made this point in a simple but powerful way: valuation has to be viewed in relation to growth.

That is also how I think about Quality Growth investing.

A company can deserve a premium multiple if it combines strong growth, high margins, high returns on capital, and a long runway for reinvestment. But the price still has to make sense relative to the future cash flows the business can generate.

And that is exactly the key question with AppLovin.

The stock was expensive at its highs. There is no way around that. But the more important question is whether the market was wrong about the company’s future earnings power — either too optimistic at the top, or now too skeptical after the sell-off.

Since its all-time high in December 2025, the stock has lost approximately 27% (as of May 26, 2026). Investors who entered at the local low of around $380 following the initial sell-off could have benefited from a discount of approximately 47%. Fortunately, I was able to time the first low on February 9, 2026 relatively accurately — which is normally not my goal and does not work reliably in practice — and build an initial position.

The stock has since risen approximately 37% from its February low and has reclaimed the long-term uptrend (red line).

Taking into account the current drivers — both positive and negative — one central question remains:

Is AppLovin’s valuation justified, and how much upside is there really?

Key Takeaways:

AXON is the entire investment case — a self-reinforcing AI advertising engine that improves with every additional data point and advertiser

Meta’s decision to stop bidding on non-IDFA iOS traffic is the strongest external validation of AXON’s moat to date

Q1 2026 was exceptional across the board: +59% revenue growth, 85% EBITDA margin, $1.29B FCF from $1.84B revenue

The sell-off was driven by narrative risk (short sellers, SEC investigation), not deteriorating fundamentals

Multiple near-term growth catalysts: AXON public launch (June 2026), consumer vertical scaling, lead generation, connected TV

The implied growth priced into the stock is significantly below the five-year historical trajectory across FCF, revenue, and EBIT

Valuation is not cheap, but not extreme — risk-reward is broadly balanced; the thesis hinges on AXON’s durability

AppLovin ranks among the highest-quality companies in my framework

Contents:

I. Why the Stock Sold Off

II. Why AXON Is the Core of the Thesis

III. What is already priced in?

IV. Latest Numbers: Still Exceptional

V. Future Prospects & Growth Drivers

VI. Valuation

VII. Risk Factors

VIII. Thesis / Classification

I. Why the Stock Sold Off

AppLovin’s sell-off cannot be explained by weak numbers alone.

That is the first important point.

The company continued to report very strong growth, margins remained unusually high, and free cash flow generation was still exceptional. This was not a case where the business suddenly missed expectations and the market simply reacted to deteriorating fundamentals.

The pressure came from somewhere else.

It came from a growing debate around the quality, sustainability, and legitimacy of AppLovin’s growth engine.

And that makes the situation much more interesting.

1. Short Sellers Went After the Core of the AppLovin Story

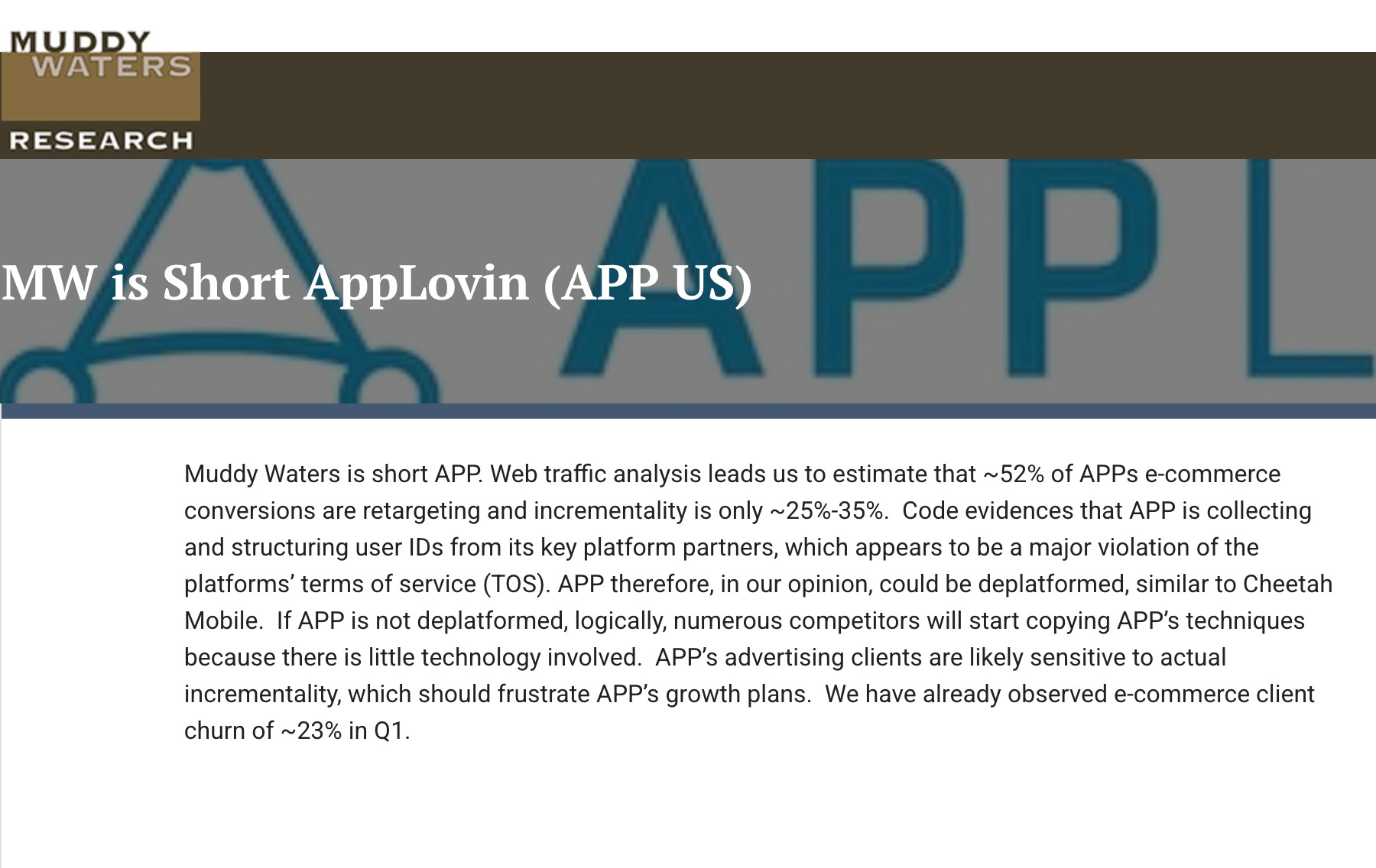

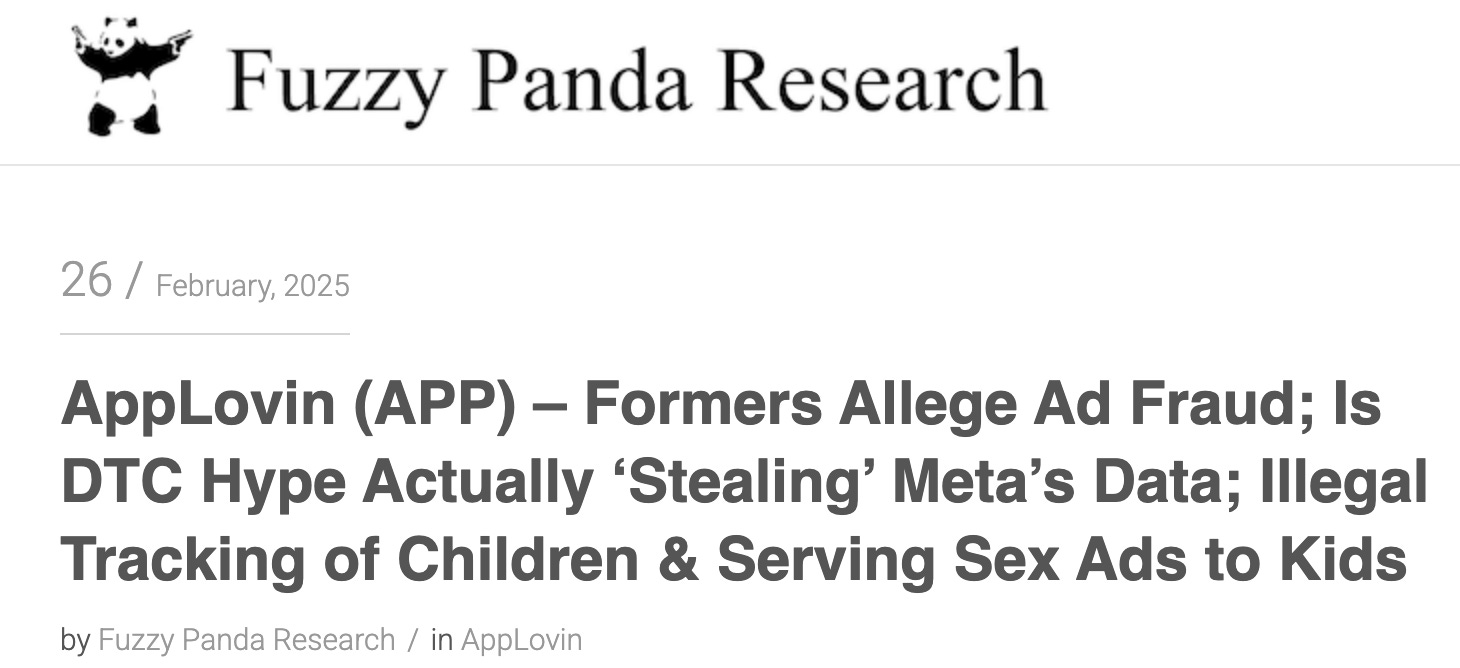

The most important driver behind the sell-off was the wave of short-seller attacks.

This was not just one report questioning valuation or arguing that the stock had run too far. Several short sellers raised much more fundamental concerns. Their reports focused on AppLovin’s advertising practices, data usage, app-install mechanics, and the way AXON allegedly achieves its performance advantage.

That matters because these accusations did not attack a side issue.

They attacked the center of the bull case.

AppLovin is not valued like a normal advertising company. The market has been willing to give the company a premium valuation because AXON appears to be an unusually powerful AI-driven advertising engine. The entire investment case is built around the idea that AXON can deliver better returns for advertisers, attract more ad spend, improve with more data, and eventually scale beyond mobile gaming.

So when short sellers question how AXON actually works, where the data advantage comes from, and whether AppLovin’s practices are fully compliant with platform rules, they are not just creating noise around the stock.

They are challenging the foundation of the story.

The basic concern can be summarized like this:

If AXON’s outperformance is purely the result of superior technology, better models, and a stronger feedback loop, AppLovin may indeed have a very powerful moat.

But if part of that performance depends on aggressive data practices, unclear user tracking, app-install tactics, or behavior that platform partners or regulators could eventually restrict, then the quality of the moat looks very different.

2. The Main Allegations Were About Data, Targeting, and Platform Rules

The short-seller concerns were not random. They focused on areas that are central to AppLovin’s business model.

Muddy Waters, for example, accused AppLovin of misappropriating data and violating the terms of service of major platform partners. The concern was that AppLovin may have been collecting or structuring user identifiers from partners in a way that could breach platform rules. Other reports raised allegations around forced or unauthorized app installations and deceptive advertising practices.

AppLovin strongly pushed back against these claims.

But even if one does not take the short reports at face value, the type of allegation is important. AppLovin operates in a part of digital advertising where data, targeting, attribution, and optimization are everything. Small differences in data access or targeting accuracy can have a large impact on advertiser returns.

That is exactly why AXON is so valuable. But it is also why the allegations matter.

If the market starts to worry that AppLovin’s advantage could be linked to practices that platform partners like Apple, Google, Meta, or regulators may challenge, then the risk profile changes. Not because the current numbers are weak, but because the durability of those numbers becomes harder to underwrite.

For a company like AppLovin, the line between “best-in-class performance marketing technology” and “too aggressive for the platform ecosystem” is incredibly important.

3. The SEC Investigation Turned Shortseller Noise Into a Real Overhang

Short reports alone often create volatility, but they do not always change the long-term story.

Many high-quality companies have faced short attacks before. Sometimes the claims are valid. Sometimes they are exaggerated. Sometimes they are simply designed to create fear around a complex business model.

The reason AppLovin’s situation became more serious is that the controversy did not stay limited to shortseller reports.

In October 2025, Bloomberg reported that the SEC was investigating AppLovin’s data-collection practices. According to Reuters, the probe focused on allegations that AppLovin may have violated service agreements with platform partners to deliver more targeted advertisements. The investigation reportedly stemmed from a whistleblower complaint and several shortseller reports.

This changed the perception of the risk.

Again, an investigation does not mean guilt. AppLovin has not been formally accused of wrongdoing. But for investors, the existence of a regulatory overhang matters because it raises the level of uncertainty.

Before the SEC headline, investors could dismiss the short reports as aggressive attacks from financially motivated actors.

After the SEC headline, the question became harder to ignore.

The market now had to consider whether regulators might also be looking at some of the same issues: data practices, targeting, platform agreements, and the mechanics behind AppLovin’s advertising performance.

That creates a different kind of pressure.

It is no longer only about whether investors believe the short sellers. It is about whether the company may face a longer period of regulatory scrutiny, limited visibility, and reputational risk.

For a premium-valued growth stock, that matters a lot.

4. The Real Issue Is Trust in AXON

The deeper reason the stock reacted so strongly is that AppLovin’s investment case depends heavily on trust.

Investors do not just need to believe that AppLovin can grow. They need to believe that the growth is high-quality, repeatable, and sustainable.

That trust is especially important because AXON is not easy to evaluate from the outside.

Investors can see the output: revenue growth, high margins, strong free cash flow, and impressive advertiser demand.

But they cannot fully see the inner mechanics of the system. They cannot independently verify exactly how AXON identifies users, optimizes campaigns, attributes conversions, or creates its performance advantage.

That makes AppLovin more difficult to analyze than a typical software company.

With a SaaS company, investors can look at retention, seat expansion, module adoption, and contract growth. With AppLovin, the key asset is a performance engine that is partly a black box. If the engine works, the numbers can be incredible. But if investors start to question the engine, the valuation becomes much more fragile.

This is why the shortseller attacks mattered.

They created uncertainty around the one thing the market needs to believe most:

That AXON’s performance advantage is real, compliant, and durable.

5. The Sell-Off Was About More Than Valuation

Valuation clearly played a role. After the huge run-up, AppLovin was priced for a lot of future success.

But I do not think valuation alone explains the sell-off.

A high valuation becomes dangerous when the story behind it becomes less certain. And that is what happened here.

The market was not simply saying:

“AppLovin is expensive.”

It was saying:

“AppLovin is expensive, and now we have to re-check the quality of the growth we are paying for.”

That is a very different situation.

If the shortseller allegations prove exaggerated and the SEC investigation does not lead to material findings, the sell-off may eventually look like a fear-driven reset. In that scenario, AppLovin’s numbers could regain control of the narrative.

But if the concerns around data practices, platform rules, or AXON’s mechanics prove more serious, then the stock’s premium valuation becomes much harder to justify.

This is why the current setup is so important.

The debate around AppLovin is no longer just about whether the company is growing fast.

It is about whether investors can trust the source of that growth.

And until that question is answered more clearly, the stock will likely remain under pressure whenever new headlines appear around short sellers, regulators, or platform practices.

II. Why AXON Is the Core of the Thesis

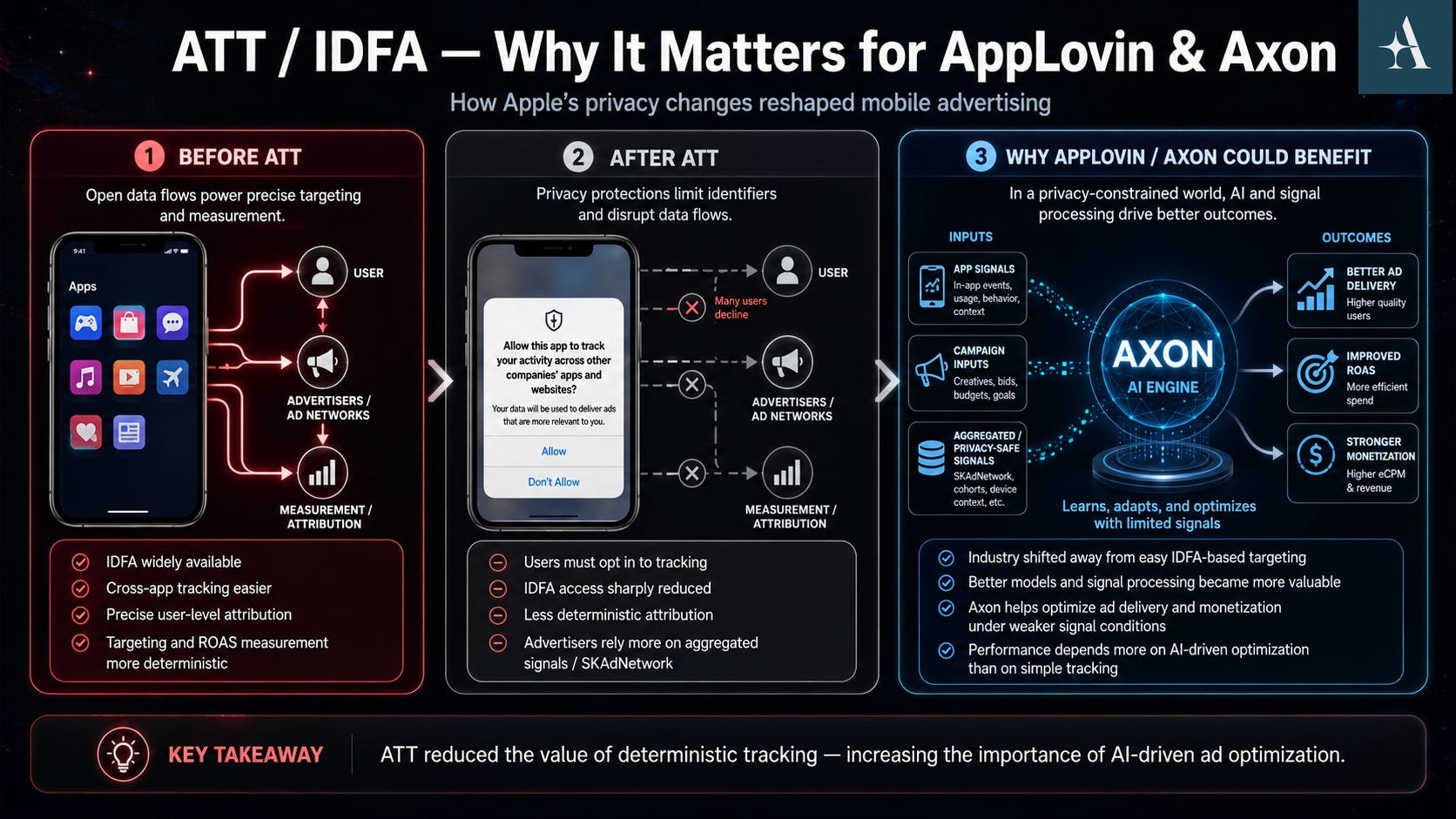

To understand why the allegations around data practices and attribution matter so much, we first need to understand what changed in mobile advertising after Apple’s ATT (App Tracking Transparency) update — and why AppLovin’s AXON engine became so important in that environment.

To understand AppLovin, you need to understand one thing: AXON.

Everything else — the high margins, the explosive revenue growth, the exceptional free cash flow generation — is the result of what AXON delivers. AXON is not a feature. It is the product. And it is the reason AppLovin today operates in a league that almost no other ad-tech company comes close to.

What AXON Actually Does

At its core, AXON is an AI-powered advertising engine that does one thing better than virtually any competitor: reaching the right user at the right time with the right ad — and doing so under conditions where others fail.

The decisive context here is Apple’s ATT framework, introduced in 2021. ATT required Apple users to explicitly consent to cross-app tracking. The result: the vast majority opted out. The IDFA — Apple’s Identifier for Advertisers, the tool that enabled precise user-level tracking — became essentially unusable for the majority of iOS traffic.

For the entire advertising industry, this was a shock. Cross-app tracking collapsed, deterministic attribution no longer worked, and advertisers suddenly had to make do with significantly weaker signals.

AppLovin and AXON built a competitive advantage precisely where everyone else showed weakness.

AXON does not use IDFA. Instead, it processes contextual signals: in-app events, usage behavior, app context, and campaign inputs. Combined with a large proprietary dataset from its own app portfolio and a model that improves with every additional signal, AXON delivers returns for advertisers that cannot be replicated through conventional tracking approaches. In a world where deterministic data has become scarce, AppLovin has built an algorithm that extracts more value from probabilistic signals than competitors can extract from direct ones.

That is not a minor optimization. That is a structural advantage.

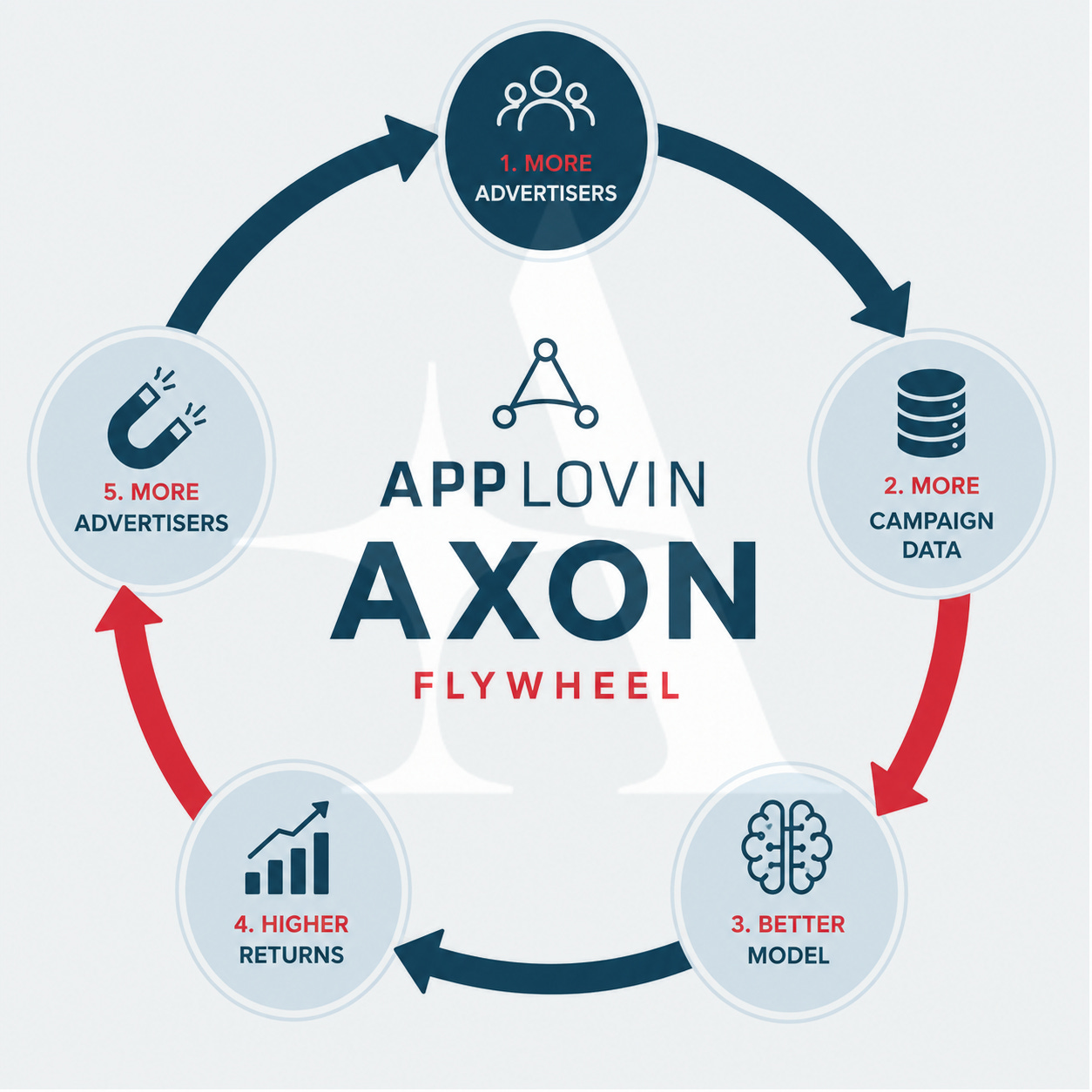

The Flywheel Effect: Why AXON Gets Stronger Over Time

What makes AXON particularly valuable is not just its current performance — it is the mechanics behind it.

More advertisers mean more campaign data. More campaign data improves the model. A better model delivers higher returns. Higher returns attract more advertisers. This is not a theoretical loop — it is what explains AppLovin’s revenue growth of 59% in Q1 2026.

This flywheel effect is the core of the moat argument. Late entrants cannot simply buy their way in with better hardware or more engineers. The advantage is accumulated: in the data, in the model iterations, in the feedback loop from millions of campaigns that AXON processes every single day.

The Latest Signal: Meta Is Stepping Back — and That Says Everything

The fact that AXON truly works is currently being demonstrated in a particularly compelling way.

According to a recent report from research firm Edgewater, Meta Platforms does not plan to bid on non-IDFA iOS traffic in the foreseeable future. That is precisely the segment where AXON dominates. Meta — one of the most powerful advertising companies in the world, with one of the largest data pools and the greatest engineering resources in the industry — apparently sees no profitable path to beating AppLovin in this space.

That is a remarkable statement.

When Meta decides not to contest this market, it is not because the market is unattractive. It is because AppLovin’s advantage there is so deeply entrenched that even a heavyweight like Meta finds the opportunity cost prohibitive. For AppLovin, this means less competitive pressure, higher margins, and a powerful signal that the competitive moat is real.

The stock reacted accordingly — rising more than 10% in a single day.

The rally continued the following day with another double-digit gain. AppLovin appears to be breaking away from its February and March lows and regaining momentum.

Why the Investment Thesis Hinges on AXON

All of this leads to one central point that every investor needs to understand.

AppLovin is not cheap. The company trades at a significant premium — and that premium is only justified if AXON delivers on what the numbers promise: a real, durable, and difficult-to-replicate performance advantage.

If AXON is what it appears to be — a self-reinforcing AI engine dominating a structurally growing market, unable to be overtaken by competitors, and improving with every additional data point — then AppLovin is one of the most interesting companies in global technology.

And Meta’s decision not to even enter the fight may be the strongest single argument one can find for that thesis.

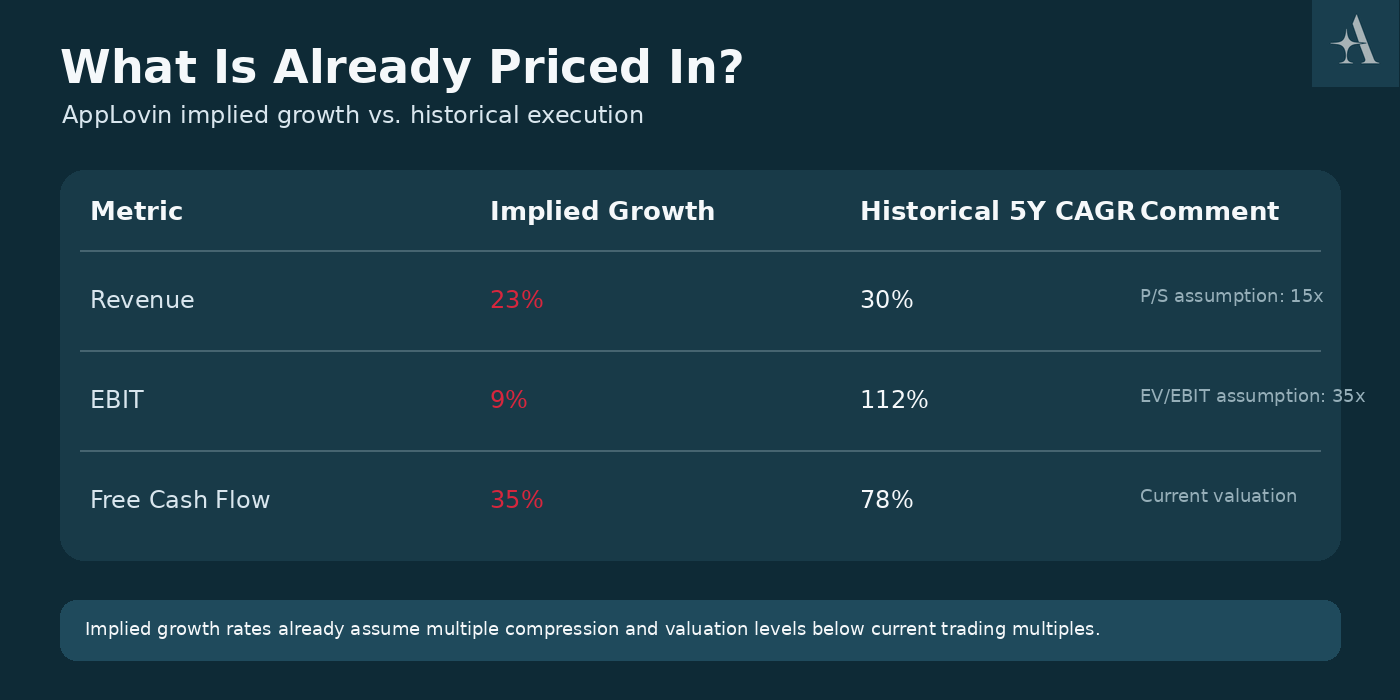

III. What Is Already Priced In?

Before looking at the latest results, it is worth asking a simple question:

What exactly is the market already expecting from AppLovin?

After all, a stock can be a great business and still be a poor investment if expectations become unrealistic. The recent sell-off has certainly reduced some of the optimism surrounding AppLovin, but the market is still pricing in a company that can grow at exceptional rates for years to come.

Consensus estimates continue to call for strong growth across revenue, earnings and free cash flow over the coming years. In other words, investors are not buying a turnaround story. They are buying the belief that AXON can continue scaling, that AppLovin can successfully expand beyond gaming, and that the company can maintain its unusually attractive combination of growth and profitability.

However, analyst estimates only tell part of the story.

To better understand what is embedded in today’s share price, I use a reverse valuation framework. Rather than estimating what AppLovin should be worth, I work backwards from the current valuation and calculate the growth rates required to justify it. This allows me to compare market expectations with both historical performance and my own assessment of the business.

Based on my calculations, the market is currently implying the growth rates shown below.

At first glance, these expectations may seem demanding. Yet an interesting picture emerges when they are compared to AppLovin’s historical execution.

The market is currently pricing in roughly 23% annual revenue growth, 9% EBIT growth, and 35% free cash flow growth over the coming years. Importantly, these estimates already assume multiple compression, using valuation multiples below current trading levels.

While past performance is never a guarantee of future results, all three implied growth rates remain below the growth AppLovin has delivered over the last five years.

This does not mean the stock is cheap. Far from it.

But it does suggest that AppLovin may not be priced for perfection either. The market is still expecting exceptional execution, yet the embedded assumptions appear more reasonable than many investors might expect at first glance.

Ultimately, the debate around AppLovin is not whether growth will continue. The real question is whether AXON can remain a durable competitive advantage and allow the company to outperform the expectations already embedded in today’s share price.

With that framework in mind, let’s turn to the latest quarter and assess whether AppLovin is currently tracking ahead of, in line with, or below those expectations.

IV. Latest Numbers: Still Exceptional

AppLovin Q1 2026: AXON Keeps Delivering

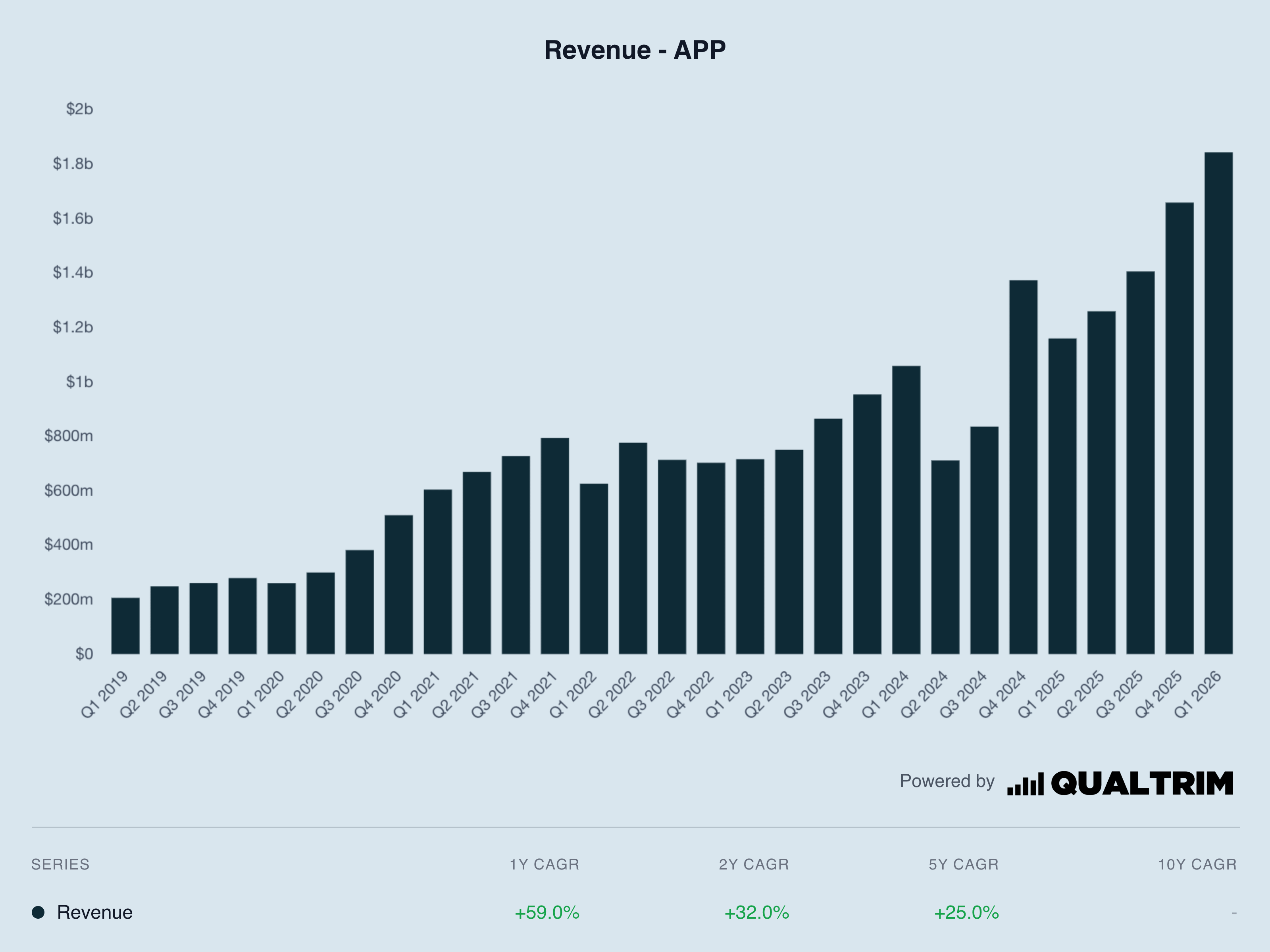

AppLovin once again reported exceptionally strong results in Q1 2026. Revenue grew 59% year-over-year to $1.84 billion, while net income more than doubled, rising 109% to $1.21 billion. More importantly, operating leverage remains extremely powerful. Adjusted EBITDA came in at $1.56 billion, corresponding to an adjusted EBITDA margin of 85%.

Key highlights:

Revenue: $1.84B, +59% YoY

Net Income: $1.21B, +109% YoY

Adjusted EBITDA: $1.56B, +66% YoY

Adjusted EBITDA Margin: 85%

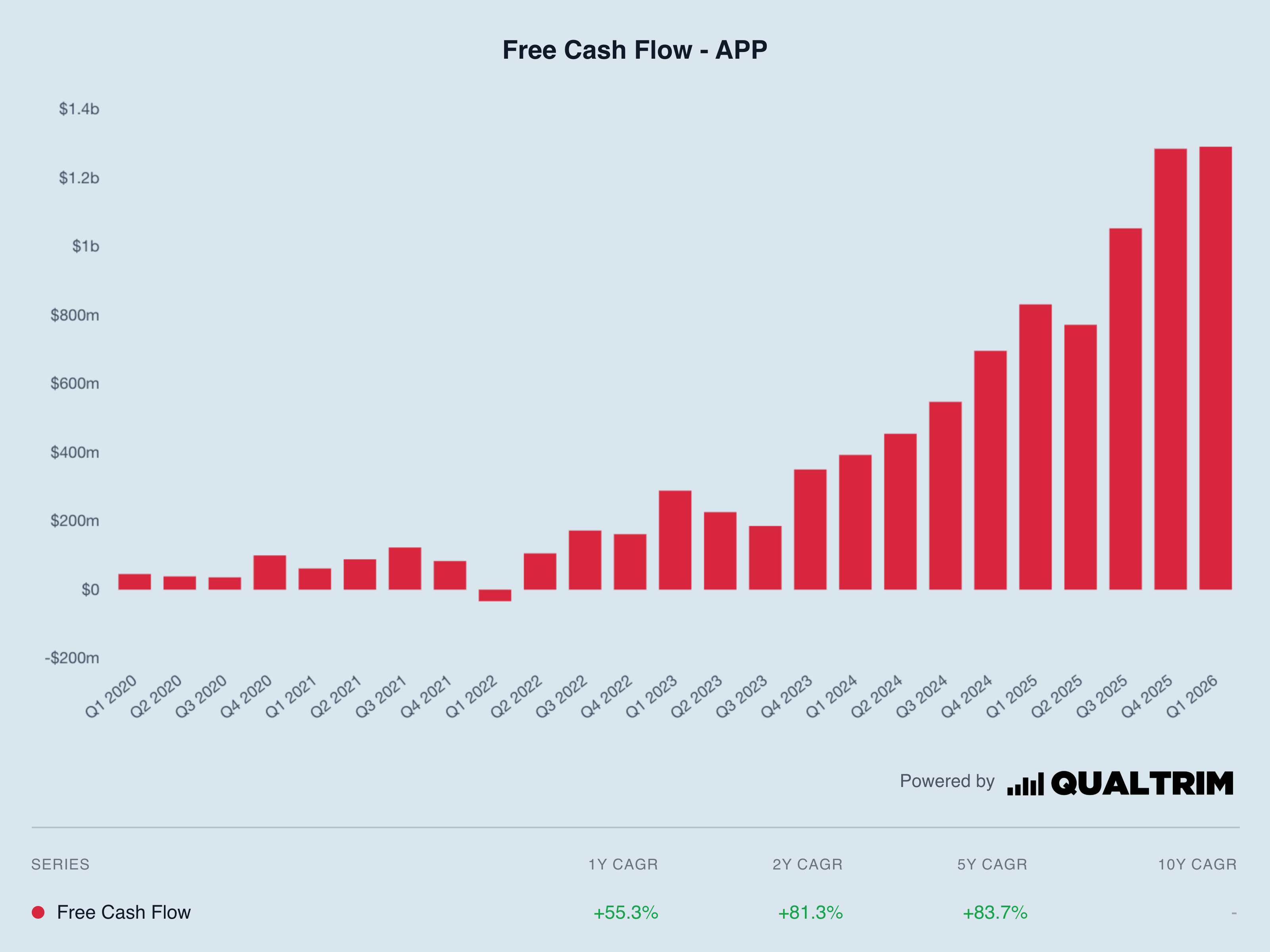

Free Cash Flow: $1.29B

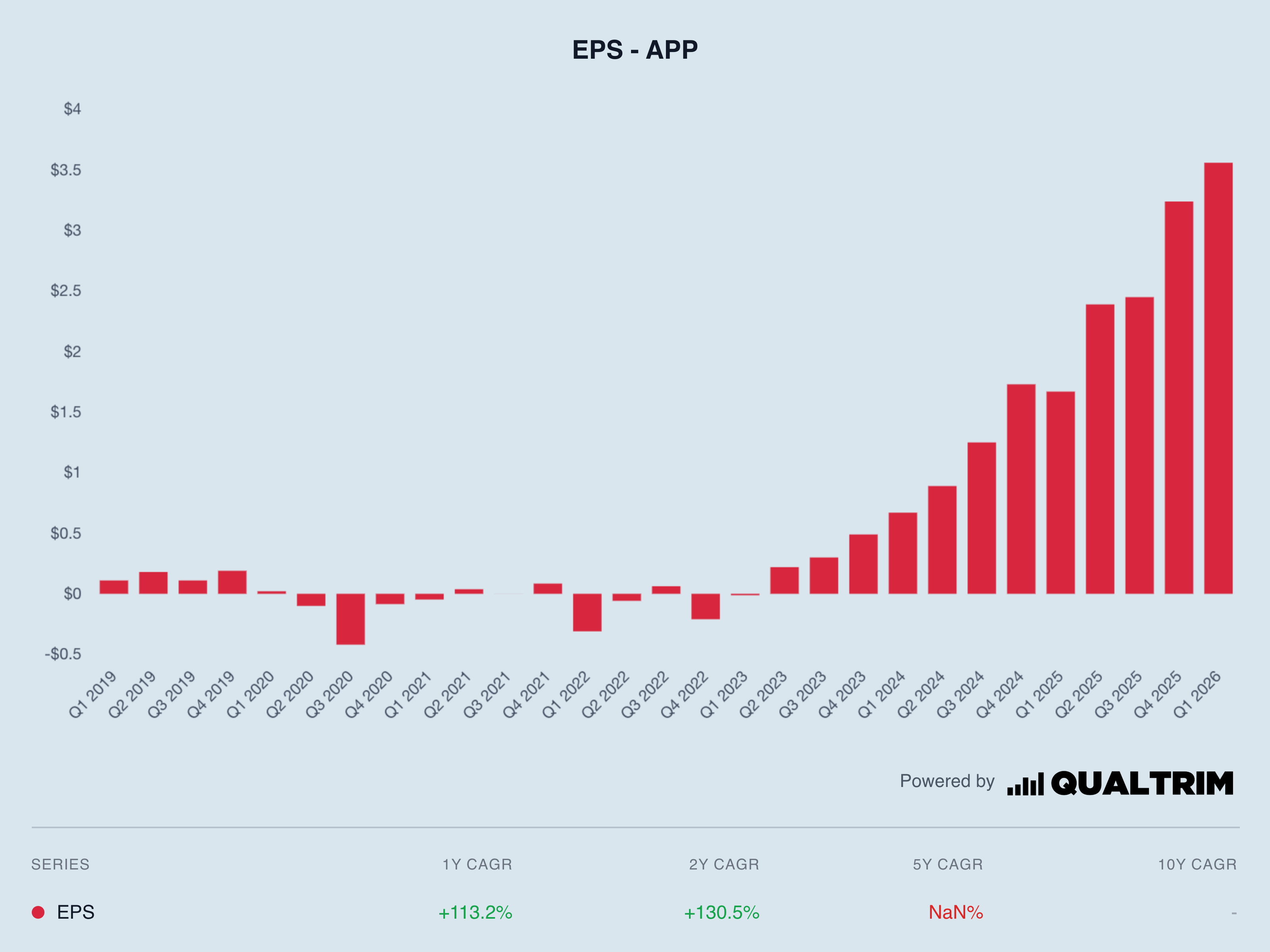

Diluted EPS: $3.56

Shareholder Returns: 2.2 million shares repurchased or withheld, total value approximately $1.0B

Cash Position: $2.76B at quarter-end

Particularly impressive is the free cash flow generation. AppLovin converted $1.84 billion in revenue into nearly $1.29 billion in free cash flow. This demonstrates just how exceptionally capital-light and margin-rich the model has become. At the same time, the company reduced shares outstanding from 338.3 million to 336.3 million compared to year-end 2025, while the cash position continued to grow despite approximately $1 billion in capital returns.

The outlook also remains strong. For Q2 2026, AppLovin expects revenue of $1.915 to $1.945 billion and adjusted EBITDA of $1.615 to $1.645 billion. The implied adjusted EBITDA margin is again 84–85%. This signals that the strong profitability is not a one-time effect, but remains structurally embedded in the business model.

Growth Rates Remain at a Very High Level

The Q1 2026 numbers were strong and confirm the long-term picture. Zooming out one level, things look no less impressive.

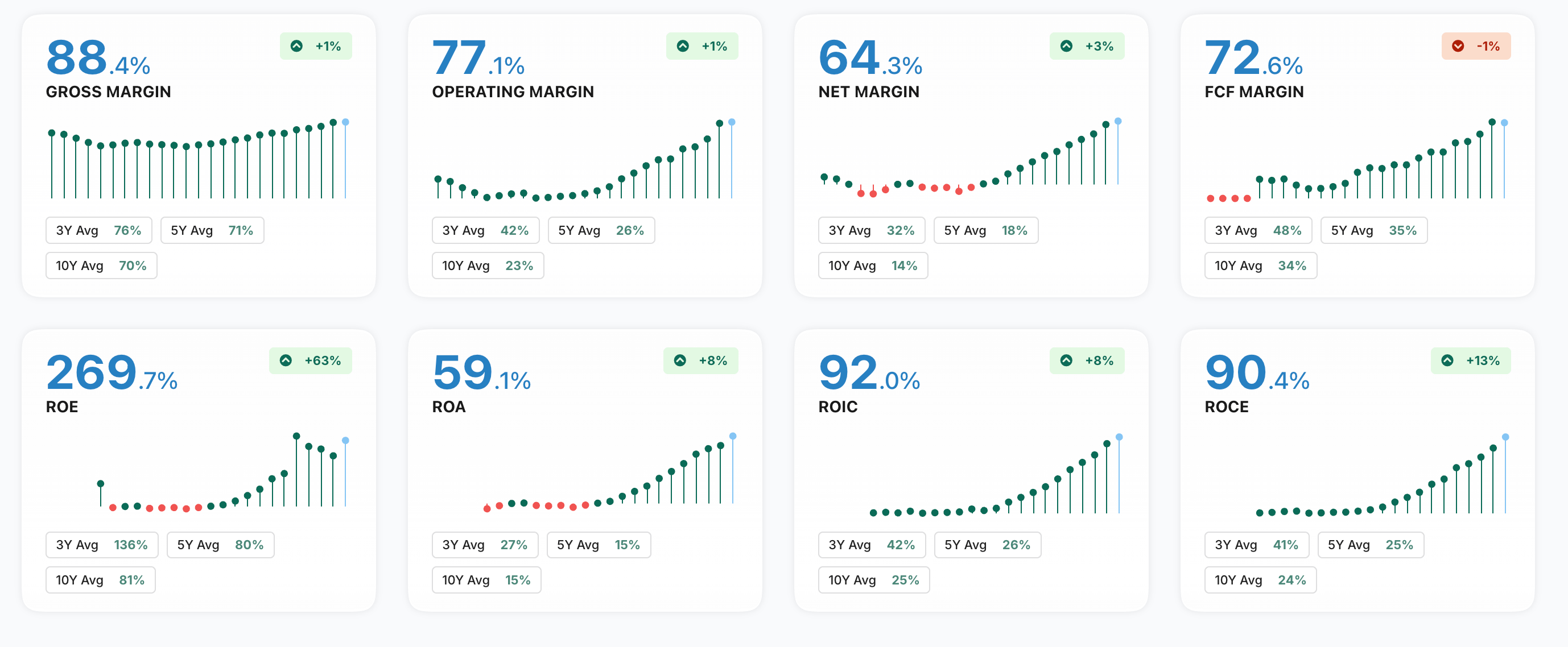

On the revenue side, a consistent upward trajectory is visible across recent quarters and years, with annual revenue growth of +32% over the last three years and +25% over the last five years. These rates are somewhat dampened by revenue stagnation in 2022 and a decline in 2023, both driven by the recession that followed the COVID-19 pandemic.

A similar trajectory is visible in net income and EPS. However, AppLovin only became consistently profitable from 2023 onwards. The annualized growth since then is impressive, standing at +130% over the past two years. Profitability has therefore been expanded significantly from that base. Net income is a metric that can be influenced by accounting effects and does not always fully reflect true underlying profitability. Stock-based compensation packages, for example, can meaningfully reduce reported net income even though no actual cash has left the business. This dilution of existing shareholders should not be ignored — it plays an important role — yet it is common practice at fast-growing companies and particularly prevalent in the software sector.

Accounting effects of this kind have clearly played a role at AppLovin as well. While net income was negative prior to 2023 — meaning the company officially reported losses — free cash flow was already positive. In simple terms: at the end of each quarter or year, the company was bringing in more cash than it was spending.

FCF is a central metric for me, because unlike net income, it is not easily manipulated and therefore provides a true picture of how much cash the company has generated at the end of a given period — after all cash outflows — which can then be deployed for purposes such as share buybacks, investments, debt repayment, or dividends.

It is important to note, however, that FCF is a liquidity metric, not a profitability metric — unlike net income. Net income is more appropriate for assessing the economic earnings power of a business over a given period, because it accounts for expenses, including certain costs and non-cash items such as depreciation, on an accrual basis. Compared to FCF, net income is also less susceptible to changes in receivables, inventory, or payables.

Both metrics are therefore highly relevant for a complete assessment of a company’s earnings situation.

Returning to FCF specifically — strong growth has also been recorded here across recent quarters and years. The five-year annualized growth rate stands at +83.7%. The ability to generate cash continues to expand.

Profitability That Is Hard to Match

Moving from growth to profitability and efficiency: revenue growth rates above 50% and earnings growth of over 100% are genuinely impressive. As I have outlined in my strategy article, growth without profitability is worth very little. For sustainable value creation, it is essential that a company converts its growth into profits and cash. AppLovin appears to be achieving this at a truly exceptional level.

Have you ever seen something like this?

Looking at these numbers, I am genuinely impressed. Profitability of this caliber is rare. The only company I can currently think of that delivers similarly strong figures is NVIDIA.

These numbers speak for themselves. What is there to criticize?

To illustrate: for every $100 AppLovin brings in, $64 flows through to net income. Many companies do not even achieve a gross margin of 64%.

Even more remarkable are the Return on Equity (ROE) and Return on Invested Capital (ROIC), both exceeding 90%. ROIC extends ROE by incorporating debt. Think of it this way: every dollar of deployed equity and debt capital generates a return of over 90%. If the company puts $100 of its equity to work, it generates an additional $90 in return.

It is always important to view capital returns in relation to the cost of capital. When returns exceed costs, a company creates value for its shareholders. AppLovin’s cost of capital (WACC) stands at just above 8%. Compared to a ROIC of over 90%, the resulting spread — also referred to as Economic Profit — exceeds 80%. That spread is extraordinary, and it represents an incredible amount of value creation.

The company is also continuing to expand this metric from an already elevated base. Since 2022, ROIC has climbed from -2% to over 90% today.

We will address the debt situation in more detail shortly. Worth noting in this context, however, is that Return on Assets (ROA) is also at a very high level. This matters because ROA needs to exceed the cost of debt — otherwise the Return on Equity deteriorates. At AppLovin, with a 60% ROA and a ROE above 90%, that is clearly not an issue — which is a very positive signal.

Combining Growth and Profitability in One Metric: Rule of 40

Based on the full-year 2025 results, the Rule of 40 stands at approximately 150 — a level that exceeds the usual frame of reference entirely.

The metric is the sum of revenue growth and operating profit margin (EBITDA) and is particularly relevant for software companies like AppLovin.

Typically, a level of 40 is considered the target and is regarded as impressive in its own right. AppLovin far exceeds that threshold, reflecting the combination of high growth rates and strong profitability.

Credit Quality Has Improved Significantly

Key metrics at a glance:

Altman Z-Score: >22

Interest Coverage: >20×

Cash Ratio: >1.8

Quick Ratio: >2.2

Current Ratio: >3.3

Long-term Solvency: 0.8

Debt/Equity: 1.6

Net Debt: $700M

The Altman Z-Score above 22 is highly positive. It estimates the statistical probability of corporate insolvency within the next two years. A score above three is generally considered low-risk.

AppLovin also comfortably clears the cash, quick, and current ratio thresholds. These indicate how many times a company can cover its short-term liabilities with its cash balances (cash ratio), cash and accounts receivable (quick ratio), or total current assets (current ratio). With all values above one, AppLovin could service its short-term obligations at any point in time.

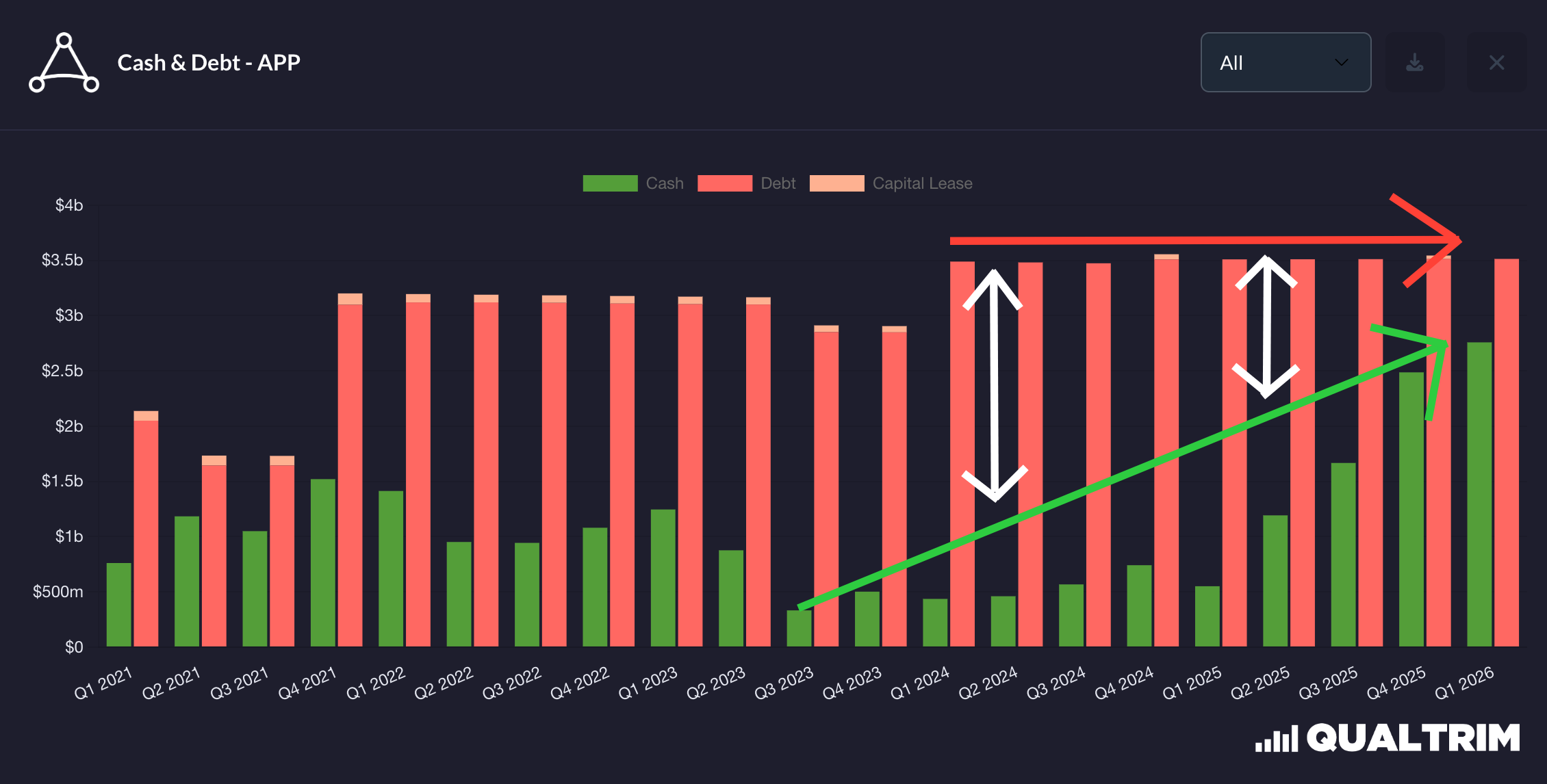

The net debt figure does illustrate that long-term debt continues to play a meaningful role — the company holds approximately $2.8 billion in cash and $3.5 billion in debt, resulting in a net debt position of $0.7 billion.

The debt-to-equity ratio above one means that long-term debt also exceeds equity, which is a less favorable signal. A ratio below one would be optimal.

Net debt is a metric I have been monitoring at AppLovin for some time. What is very encouraging, however, is that over the past two years the company has taken on virtually no new debt while simultaneously building its cash balances significantly. This is where the exceptional profitability becomes tangible. The debt was necessary to lay the groundwork for strong growth — but with the high profit margins the company now generates, taking on additional leverage no longer appears necessary. AppLovin is now able to finance its investments internally, while retaining enough cash to continue building its reserves.

This chart therefore captures a genuinely decisive development:

AppLovin is a company of exceptional quality.

I have developed a proprietary scoring framework for my strategy, designed to identify the best quality-growth companies. It combines quantitative metrics — such as those outlined above — with qualitative factors including moat strength and innovation capacity.

AppLovin firmly belongs in that category.

As a result, the compounder receives 130.1 out of a possible 140 points and is rated “Top-Quality.”

V. Future Prospects & Growth Drivers

1. Public Launch of AXON in June 2026

Adam Foroughi, CEO & Co-Founder:

“Come June, advertisers across the world will be able to sign up for Axon and start running campaigns.”

For 14 years, AppLovin has operated as a closed platform. That changes in June 2026 — and this is not an incremental update. It is a structural break in the company’s history. For the first time, advertisers worldwide will be able to register for AXON and launch campaigns independently, without going through AppLovin’s direct sales process. Foroughi has already quantified what this could mean: if 100,000 new customers are acquired in the first year — and the average annual value per new customer exceeds $70,000 — that translates to approximately $7 billion in additional advertiser spend from this initiative alone.

2. Consumer Vertical as the Next Major Growth Engine

Adam Foroughi, CEO & Co-Founder:

“The consumer vertical is scaling fast and we are just getting started.”

The consumer segment — initially launched as an e-commerce product — is only about one and a half years old. And yet it is already growing faster than the gaming business AppLovin spent over a decade building. March 2026 came in approximately 25% above the January level, and April was the strongest month in the vertical’s history — stronger than any Q4 month prior. That is notable because Q4 is seasonally the strongest period in the advertising industry. The fact that AppLovin surpassed that benchmark as early as April, before the platform has even opened to the public, illustrates the scale of the opportunity that is only just beginning to be unlocked.

3. Model Improvements as the Core of Growth

Adam Foroughi, CEO & Co-Founder:

“As we add more advertisers, we get more data.”

The decisive mechanism behind AppLovin’s growth is not a conventional sales success story — it is a self-reinforcing cycle, as depicted above. More advertisers deliver more data. More data improves the model. A better model generates higher returns for advertisers. Higher returns attract more budget. Foroughi describes this process on the earnings call as a direct analogy to LLM development: continuous model updates that lift everything simultaneously — both gaming and consumer. The latest major release, just a few weeks before the Q1 call, was described by Foroughi as “quite substantial” and directly explains the acceleration seen toward the end of the quarter.

4. Gaming Remains a Structural Growth Driver

Adam Foroughi, CEO & Co-Founder:

“We have 100% seen faster improvements to the models.”

Gaming is the foundation on which everything else is built — and it is not weakening. Since the launch of AXON 2.0, AppLovin has delivered twelve consecutive quarters of growth without a single deceleration. What further fuels the gaming segment is that AI tools are dramatically reducing development costs for studios. Established publishers can improve existing games faster and now have the confidence to launch new titles. The result is a wave of new, high-quality content — directly in the format where AppLovin is strongest: hybrid monetization combining ads and in-app purchases.

5. More Consumer Demand Also Improves Gaming Supply

Adam Foroughi, CEO & Co-Founder:

“We haven’t yet, since we launched Axon 2.0, seen a slowdown.”

At first glance, one might worry that growing consumer demand would cannibalize the gaming segment — after all, both compete for the same impressions. But the opposite is true. AppLovin currently wastes a considerable share of its impressions showing gaming ads to users for whom a different ad would be more relevant. The more consumer brands are active on the platform, the more precisely the model can determine which ad has the highest conversion probability at any given moment. Greater advertiser density increases competition within the auction system, driving eCPMs higher — and publishers in the gaming segment ultimately benefit from that as well.

6. AI Creative Tools Lower the Barrier to Entry for New Advertisers

Adam Foroughi, CEO & Co-Founder:

“We’ll hand it to them with these tools.”

One of the biggest friction points in onboarding new advertisers has historically been creative assets. AppLovin’s ad format is unique: over 30 seconds of uninterruptible attention — a format for which conventional social media ads simply do not work. Many prospective advertisers were not deterred by lack of interest, but simply by the absence of suitable video material. With the AI-generated Interactive Page Generator — already broadly rolled out — and a video generator approaching full launch, AppLovin is solving this problem directly. The gap between “platform discovered” and “first campaign live” is being reduced to a minimum. That is precisely what a self-serve platform launch in June requires.

7. Lead Generation as an Additional TAM Expander

Adam Foroughi, CEO & Co-Founder:

“We’re missing a huge category: leads.”

AppLovin currently serves advertisers who measure direct transactions — e-commerce, apps, games. But a vast segment of the digital advertising market is structured differently: insurance, financial services, food delivery, real estate. These industries do not buy sales — they buy leads. Foroughi identifies this as one of the largest untapped categories for AppLovin — comparable to where the consumer vertical stood when it launched six quarters ago. A working cost-per-lead model would give AppLovin access to advertiser budgets that are structurally excluded today. Testing is already underway.

8. Connected TV as a Long-Term Option

Adam Foroughi, CEO & Co-Founder:

“Television is massively undermonetized.”

Connected TV is not a near-term growth driver — Foroughi says so explicitly. But the strategic logic is clear and compelling: television advertising today is almost exclusively a branding tool for large companies. Small and mid-sized businesses have no access to the big screen — and when they do, they can barely measure return on investment. AppLovin’s vision is to transpose the same performance marketing approach that worked in mobile gaming onto the television screen. Advertisers already scaling on AXON could expand their campaigns to Connected TV with a single click — including AI-generated creative and measurable ROAS. Wurl, AppLovin’s CTV asset, is the technological foundation for this. It is still early days. But if it works, it represents a massive TAM expansion.

VI. Valuation

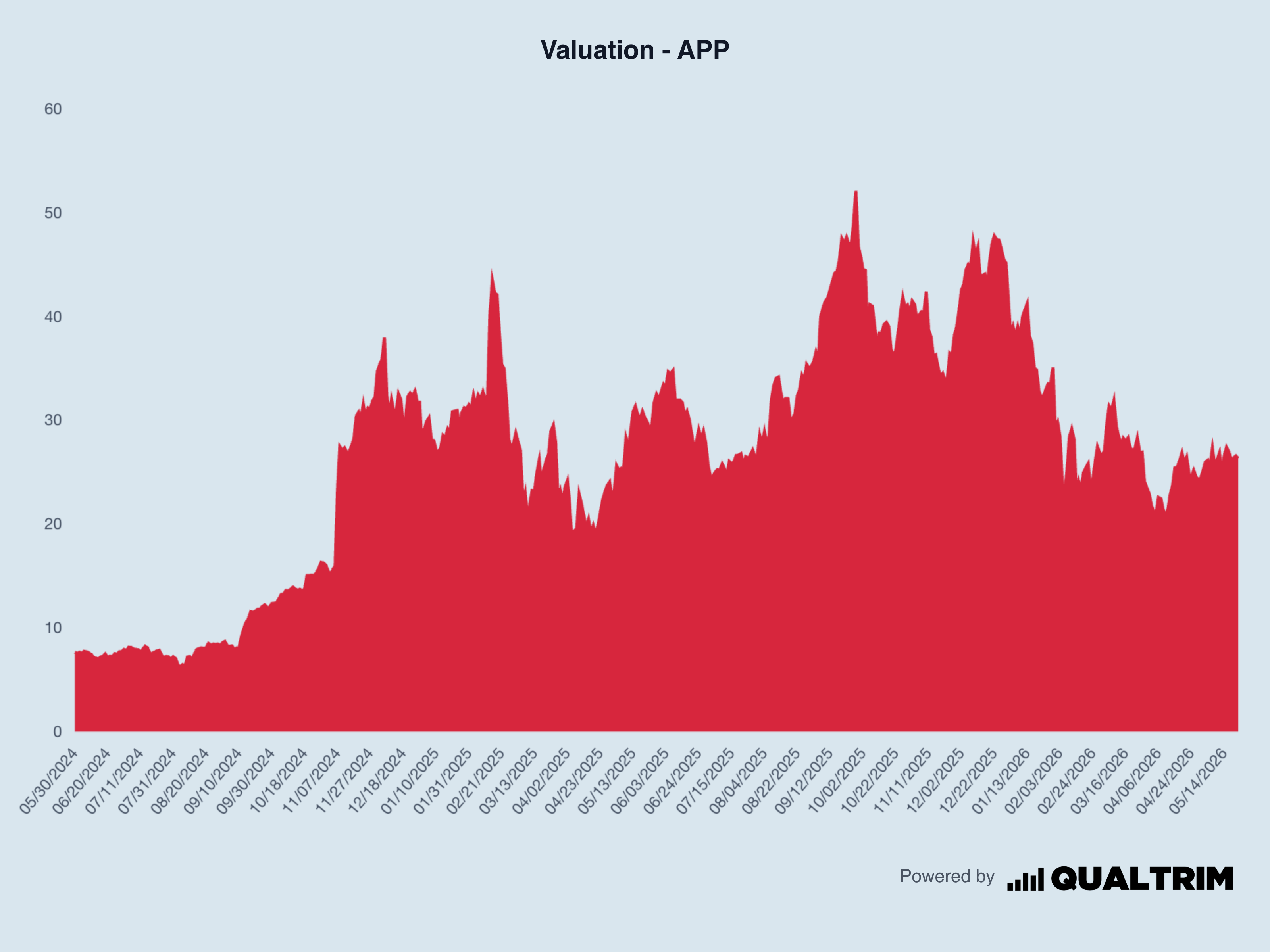

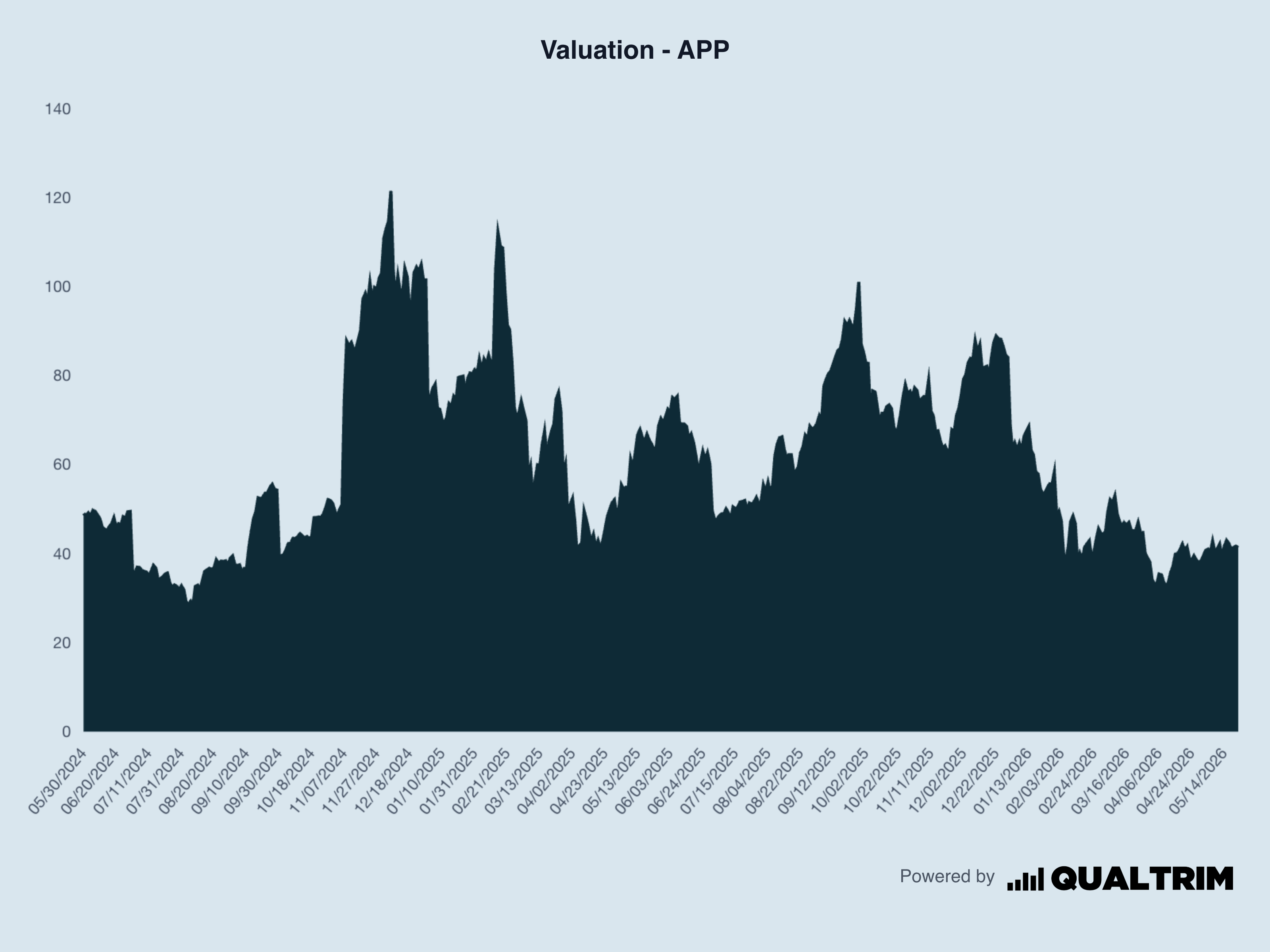

AppLovin is expensive.

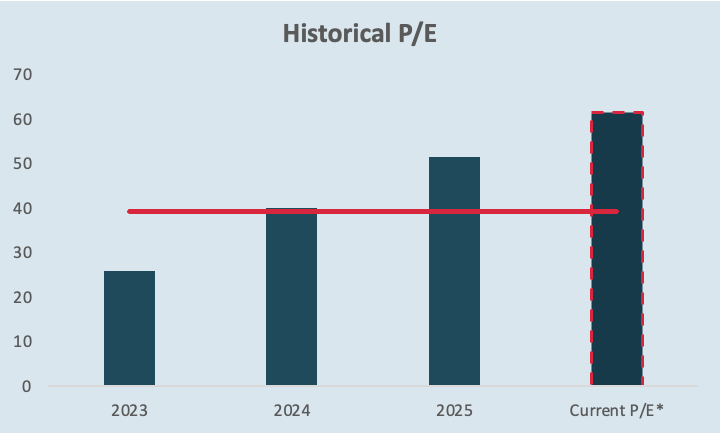

P/E TTM: 41

P/E based on 2025 EPS: 61

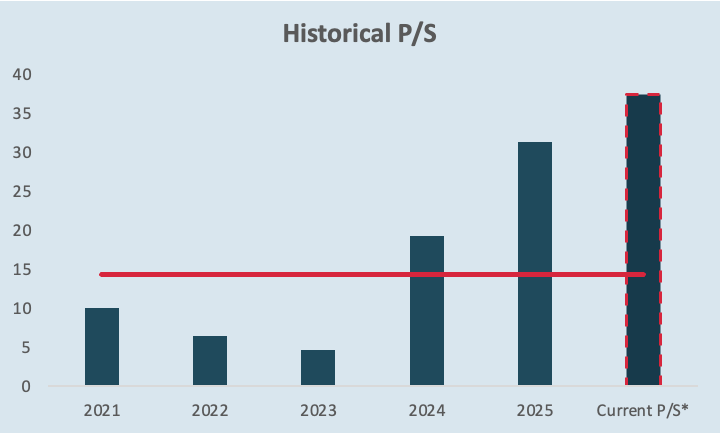

P/S: 32

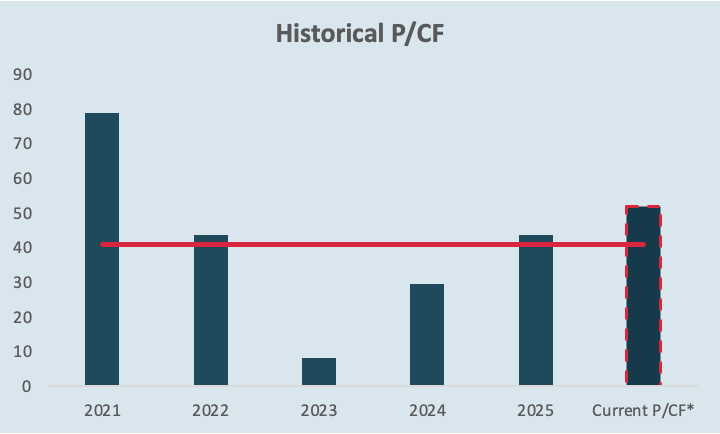

P/CF: 52

Viewed in isolation, these are undeniably elevated levels.

Which is precisely why rule number one in valuation applies here: these metrics should never be viewed in isolation.

When each figure is related to the respective projected growth for the coming year, the picture looks as follows:

PEG Ratio (TTM P/E): 1

P/S to Growth: 0.91

P/CF to Growth: 1.75

A PEG ratio at or below 1 and a P/S to Growth ratio at or below 0.5 are considered attractive.

Development of P/S-Ratio:

Development of P/E-Ratio:

At the P/S ratio level, the current figure sits above the average of recent years, while the P/E ratio is approximately in line with its historical average.

The forward P/E for the next twelve months, however, is only 27.8 — a historically low level. For 2027, it is projected to fall further to just 22.53.

Looking at AppLovin’s historical valuation multiples, a consistent pattern emerges.

The stock currently trades above its historical averages across P/S, P/E and P/CF. This should not come as a surprise. Investors are assigning a premium valuation to a business that has significantly improved its profitability, free cash flow generation and capital allocation over the past several years.

At the same time, the valuation is not entirely disconnected from fundamentals. Unlike many high-growth companies, AppLovin combines rapid growth with exceptional margins and substantial free cash flow generation. As a result, a higher-than-average multiple may be justified if the company can continue executing at a high level.

Taken together, the valuation picture is more nuanced than headline multiples might suggest.

On an absolute basis, AppLovin is undoubtedly expensive. The stock trades at a premium to both the broader market and its own historical averages across most valuation metrics.

However, valuation should always be viewed in the context of growth, profitability and future earnings power. AppLovin continues to combine exceptional revenue growth with industry-leading margins and substantial free cash flow generation — a combination that is rarely available at bargain prices.

The key question is therefore not whether AppLovin is cheap today. It isn’t.

The real question is whether AXON can continue to compound the company’s earnings power at a rate that justifies the premium valuation. If it can, today’s multiples may look far less demanding in hindsight. If it cannot, the stock leaves little room for disappointment.

VII. Risk factors

A concise overview of the most important risk factors:

SEC investigation / regulatory overhang: The investigation into data practices reportedly remains active according to Reuters/Bloomberg; AppLovin has not yet been formally accused of any wrongdoing.

Short-seller allegations / trust risk: Multiple short sellers have targeted AppLovin over alleged data and tracking practices, platform rule violations, and AXON mechanics.

Platform dependency: Apple, Google, Meta, and app stores can change rules around tracking, attribution, ads, and app distribution.

AXON durability risk: The thesis depends on AXON sustainably delivering superior performance — not just temporarily.

Expansion beyond gaming: The market is increasingly pricing in AppLovin’s ability to scale into consumer, e-commerce, and additional verticals.

Valuation risk: Despite the sell-off, the stock is not cheap; disappointing growth could trigger a sharp multiple contraction.

Margin normalization: AppLovin’s margins are exceptionally high; any normalization would weigh on the valuation.

Customer concentration / advertiser ROI risk: If advertisers do not see a clear ROAS, budgets can shift away quickly.

Reputation risk: Even unproven allegations can weigh on perception, because trust is part of AppLovin’s moat.

Macro & advertising spending risk: AppLovin ultimately depends on advertising budgets. Economic slowdowns, weaker consumer spending, or reduced marketing investments could pressure growth, even if AXON continues to outperform competitors. Performance advertising tends to be more resilient than brand advertising, but it is not immune to a weaker macro environment.

VIII. Thesis / Classification

AppLovin ranks among the highest-quality businesses in the market by virtue of its fundamental strength.

The recent discussions around the business model and the AXON algorithm sound concerning, but are based on allegations and hypotheses. None of it is definitively proven. Short sellers naturally have a financial interest in their publications gaining traction and driving prices lower. Short reports are therefore often written in a particularly negative tone to generate adverse sentiment — and in doing so, reality is frequently distorted or presented in a more extreme light than the facts warrant. For this reason, I would not ignore such reports, but I would absolutely scrutinize them critically and form my own judgment.

The SEC investigation should naturally be taken more seriously than the short reports. Nevertheless, it is important to note that AppLovin has not yet been formally accused of any specific wrongdoing. There is therefore nothing to do but monitor developments. My base case is that the investigation either fades without consequence or that the company faces a financial penalty if the short sellers’ allegations contain any substance, or if the regulator identifies something else in the course of its review. I consider the probability that this matter poses a genuine structural threat to the business model to be low.

Other risks — such as dependence on major platforms like Apple, Google, or Meta, or reliance on the core growth engine, AXON — should absolutely remain on the radar. These risks carry meaningful potential to negatively alter the business model. That said, I would not overweight them at this stage. On the question of platform dependency specifically, AppLovin has demonstrated through its proprietary AI engine AXON that it can operate effectively even in a challenging regulatory environment — the ATT/IDFA framework being the key example — while sustaining high growth rates and strong profitability. In doing so, it has established a clear competitive advantage over rivals such as Meta. That speaks clearly in the company’s favor.

In my view, the most significant near-term risk is the dependence on the macroeconomic environment and the associated advertising spend risk. 2022 provided a clear illustration of what a recession can do to the APP share price — it fell approximately 90% from peak to trough, and revenue growth collapsed alongside it. That risk has not disappeared, but in my assessment it is no longer of the same magnitude as in 2022. AppLovin is today a well-established company with a market capitalization of approximately $200 billion (as of May 30, 2026). Back then, it was almost entirely dependent on the gaming business. Today, the company is actively diversifying its business model — which is a positive development. The dependence on advertising revenues persists, however, and in the event of an economic downturn, it could quickly translate into sharper share price volatility. That would not mean the business model is broken — it would mean that the macro environment is causing temporary weakness. Historically, such periods tend to offer exceptional opportunities.

Returning to the positives and the opportunity side of the equation:

AppLovin is characterized by excellent fundamentals. The strong cash generation and high profit margins, combined with impressive growth rates, are creating substantial value for both the company and its shareholders. The share buyback program has been expanded accordingly, returning a portion of capital to shareholders indirectly. This level of profitability enables the company to finance its own investment projects and expansion plans from internal cash flows — meaning long-term debt has not needed to grow further. Cash balances have increased and overall credit quality has improved. There are no concerns whatsoever regarding financial distress.

The operational and financial strength makes AppLovin more resilient in challenging environments. With respect to the macroeconomic dependency discussed above, the strong fundamental position helps the company navigate through difficult periods more effectively and limits the risk of the kind of extreme drawdowns seen in 2022.

The late-May 2026 news that Meta plans to withdraw from a core segment of AppLovin’s market has injected fresh momentum into the stock and reduced competitive pressure. Together with expansion plans beyond gaming into e-commerce, lead generation, and connected TV, as well as the opening of the platform to advertisers from June 2026 onwards, the outlook for growth is highly promising. AppLovin appears well-positioned to establish itself as a leading player in the advertising industry over the coming years — provided the expansion plans execute and AXON continues to drive strong growth.

The AI engine AXON and the auction platform MAX create high switching costs by enabling advertisers to consistently reach the right audience at the right time. The result is high engagement rates. AXON therefore represents a central competitive advantage over other providers and continues to improve through the flywheel effect described above.

From a valuation standpoint, AppLovin is in my view neither cheaply priced nor extremely expensive. The risk-reward profile appears broadly balanced. Building an initial position to participate in the company’s growth story going forward can be a sensible decision. Personally, however, I am waiting before adding more significantly, and will continue to monitor the share price as well as the fundamental and legal developments of this compounder. Over the coming years, I see further upside potential for AppLovin — though it may be accompanied by volatility. One important principle applies here: as long as the fundamentals remain strong and the thesis is intact, falling prices alone are not a reason to sell. Such situations frequently present attractive opportunities.

Ultimately, the investment case comes down to a single question: can AXON remain the superior advertising engine it appears to be today?

If the answer is yes, AppLovin’s growth runway may be significantly longer than the market currently assumes.

If you’ve made it this far — thank you sincerely for reading.

Until next time,

Finn

If you enjoy my strategy and way of thinking, and don’t want to miss future deep dives, quarterly reviews, watchlist updates, and further insights into my analysis process, consider subscribing to Antares Research.

That way, you’ll stay up to date on future opportunities, strong businesses, and attractive setups within my framework.

If you found this article valuable, I’d also appreciate you sharing it.

This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All views expressed reflect my personal opinion at the time of publication. Any investment decision should be based on your own research and judgment.